Looking to unlock the value hidden in your home? Getting home equity loan quotes is the first step to turning your property’s worth into real cash you can use.

Whether you want to renovate your kitchen, consolidate debt, or cover unexpected expenses, knowing your loan options can save you thousands. But with so many lenders and rates out there, how do you find the best deal for your situation?

This article will guide you through everything you need to know about home equity loan quotes, helping you make smart choices that protect your investment and your wallet. Keep reading to discover how to compare offers, understand key terms, and get the loan that fits your needs perfectly. Your home’s equity could be the key to your next big opportunity—let’s unlock it together.

Home Equity Loan Basics

A home equity loan lets homeowners borrow money using their house’s value. It is a one-time loan with fixed interest and set payments. Borrowers get the full amount upfront and pay it back over time.

A HELOC (Home Equity Line of Credit) works like a credit card. It lets you borrow and repay repeatedly up to a limit. The interest rate usually changes, and payments can vary.

Home equity loans use the difference between your home’s market value and what you owe. The bank holds a claim on your home until you repay. These loans often help pay for big expenses like repairs or education.

| Feature | Home Equity Loan | HELOC |

|---|---|---|

| Loan Type | Fixed amount, lump sum | Revolving credit line |

| Interest Rate | Usually fixed | Usually variable |

| Repayment | Fixed monthly payments | Flexible payments |

| Use of Funds | One-time expenses | Ongoing or flexible use |

Factors Affecting Loan Rates

Credit score greatly affects the interest rate offered. Higher scores get lower rates. Lower scores may mean higher costs or rejection.

Loan-to-value (LTV) ratio shows how much you borrow compared to home value. Lower LTV means less risk for lenders and better rates.

Loan term length changes monthly payments and total interest. Shorter terms usually have higher payments but lower rates. Longer terms have smaller payments but cost more in interest.

Market conditions like economy and interest trends impact loan rates. Rates can rise or fall based on these external factors.

Finding The Best Rates

Comparing lenders in Austin, Texas helps find the best home equity loan rates. Different lenders offer various rates and terms. Check local banks, credit unions, and online lenders for options. Pay attention to interest rates, fees, and repayment terms. These affect the total loan cost.

Using online rate quotes saves time. Many websites let you enter your details and see multiple offers. This helps compare rates quickly and easily. Look for no-obligation quotes to avoid pressure.

Negotiating with lenders can lower your rate or fees. Mention offers from other lenders to get better terms. Ask about any discounts for good credit or automatic payments. A simple conversation can improve your loan deal.

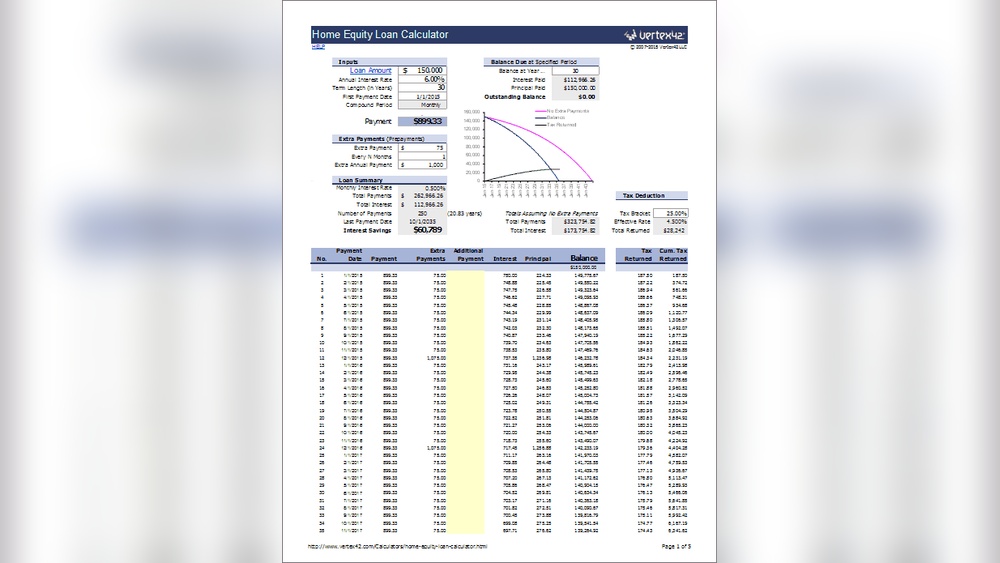

Calculators And Tools

Home equity loan calculators help estimate monthly payments and total costs. These tools show how different loan amounts and interest rates affect your payment. Payment estimators break down principal and interest to help plan your budget.

Rate comparison tools display current interest rates from various lenders. They allow you to find the best deal quickly. By comparing rates, you can save money over the loan term. These tools often update daily to provide accurate information.

| Tool | Purpose |

|---|---|

| Home Equity Loan Calculators | Estimate monthly payments and loan costs |

| Payment Estimators | Show breakdown of principal and interest |

| Rate Comparison Tools | Compare current interest rates from lenders |

Tips To Save Big

Improving your credit score before applying can lower your loan rates. Pay bills on time and reduce debts. Check your credit report for errors and fix them quickly. A higher credit score means better loan offers.

Choosing between fixed and variable rates depends on your risk comfort. Fixed rates stay the same, making payments easy to plan. Variable rates can change, sometimes going lower or higher. Decide what fits your budget best.

Hidden fees can increase loan costs. Watch out for origination fees, appraisal fees, and early payoff penalties. Ask lenders to explain all charges clearly. Comparing quotes helps spot fees and avoid surprises.

Common Uses For Loans

Home equity loans often help pay for home renovations. These loans provide funds to fix or improve a house. Upgrades like new kitchens, bathrooms, or roofs become possible.

Debt consolidation is another popular use. People combine several debts into one loan. This can lower monthly payments and simplify finances.

Many also use home equity loans for major purchases. This includes buying cars, paying for education, or covering medical bills. The loan is usually cheaper than credit cards.

Risks And Considerations

Home equity loans carry risks that borrowers must understand. The potential for foreclosure exists if payments are missed. Since the home is collateral, failure to pay can lead to losing the house.

Credit scores can be affected by late or missed payments. This can lower your ability to borrow in the future. Always keep track of your payment schedule to avoid damage.

These loans can have long-term financial effects. Monthly payments may increase your debt load. This could limit your budget for other needs or emergencies. Think carefully about your ability to repay before borrowing.

Expert Opinions

Financial advisors often see home equity loans as a useful tool. They suggest using these loans for major expenses like home repairs or education. These loans usually offer lower interest rates than credit cards. But, advisors warn about borrowing more than you can pay back.

Dave Ramsey, a well-known financial expert, strongly discourages home equity loans. He believes paying off your house should be the priority. He says borrowing against your home can lead to serious money problems.

Avoid home equity loans if you have unstable income or plan to move soon. Also, skip these loans when you use the money for non-essential spending. Using home equity loans carelessly can risk losing your home.

Frequently Asked Questions

How Much Would A $50,000 Home Equity Loan Cost Per Month?

A $50,000 home equity loan costs about $230 to $300 monthly, depending on interest rates and loan terms.

How Much Would A $300,000 Home Equity Loan Cost Per Month?

A $300,000 home equity loan monthly payment varies by interest rate and term. For a 5% rate over 15 years, expect about $2,370. Rates and terms affect costs, so use an online calculator for precise estimates.

What Does Dave Ramsey Say About Home Equity Loans?

Dave Ramsey advises against home equity loans. He encourages paying off your home fully and avoiding borrowing against it.

What Is The Monthly Payment On A $70,000 Home Equity Loan?

A $70,000 home equity loan’s monthly payment depends on the interest rate and loan term. For example, at 6% interest over 15 years, payments are about $590 monthly. Use a loan calculator to get exact figures based on your specific rate and term.

Conclusion

Finding the right home equity loan quote takes time and effort. Compare rates from different lenders carefully. Pay attention to terms, fees, and repayment options. Choose a loan that fits your budget and goals. Remember, borrowing against your home has risks.

Use your loan wisely to improve your financial situation. Stay informed and ask questions before deciding. This way, you can make a smart choice with confidence.