Thinking about tapping into your home’s value? A Property Equity Loan Estimate is your first step to understanding how much you can borrow and what your payments might look like.

Knowing these details upfront puts you in control, helping you make smarter financial decisions without surprises. You’ll discover exactly what a property equity loan estimate includes, why it matters to you, and how it can save you time and money.

Ready to unlock the potential of your home’s equity with confidence? Let’s dive in.

What Is A Property Equity Loan Estimate

A Property Equity Loan Estimate shows the expected costs and fees of a loan. It helps homeowners understand how much money they can borrow using their home’s equity.

The estimate includes details like loan amount, interest rate, monthly payments, and closing costs. It also shows the annual percentage rate (APR) to compare different loans easily.

Receiving this estimate lets homeowners plan their budget better. It clarifies what to expect before signing any agreement. This helps avoid surprises later.

Loan estimates are usually given by lenders after applying for a home equity loan. They follow strict rules to ensure clear and honest information.

How Lenders Calculate Equity Loans

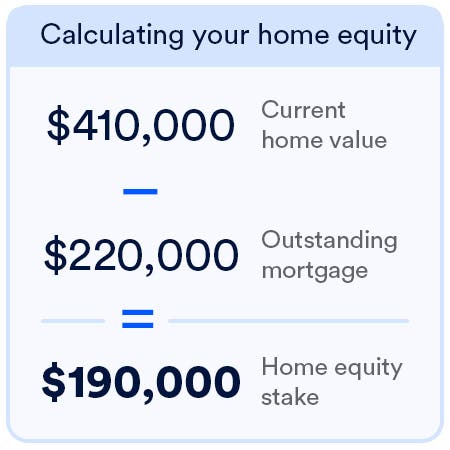

Lenders use several key factors to decide your equity loan amount. The Loan-to-Value (LTV) ratio is crucial. It compares your loan balance to your home’s value. A lower LTV means more equity and a better chance for a loan.

Credit scores affect loan approval and rates. Higher scores usually get better terms. Scores below certain limits might lead to higher interest rates or loan denial.

| Factor | Effect on Loan |

|---|---|

| Loan-to-Value Ratio | Lower ratio = higher loan amount possible |

| Credit Score | Higher score = better interest rates and terms |

| Interest Rates and Terms | Rates depend on market and credit profile; terms vary by lender |

Interest rates impact monthly payments. Fixed rates keep payments steady. Variable rates can change over time. Loan terms can be short or long, affecting total cost.

Using Home Equity Loan Calculators

Home equity loan calculators help estimate how much money you can borrow. You enter key inputs like your home’s value, current mortgage balance, and credit score. These details show the maximum loan amount and monthly payments you might expect.

Interpreting results is simple. Look for loan amount, interest rate, and monthly payment. These numbers help you decide if the loan fits your budget. Some calculators also show the total cost over the loan term.

| Popular Calculator Tools | Features |

|---|---|

| Calculator.net | Loan amount, monthly payment, interest, APR |

| Bankrate | Borrowing limits, payment estimates |

| U.S. Bank | Monthly payments, APR for loans and HELOC |

| Bank of America | Payment estimates based on loan amount and rates |

Benefits Of A Property Equity Loan

A property equity loan usually offers lower interest rates than other loans. This helps save money on monthly payments. Interest is often tax deductible, which can reduce the amount of tax owed. This makes borrowing cheaper overall.

These loans let you access large funds by using your property’s value. It is useful for big expenses like home repairs, education, or debt consolidation. Borrowing this way can be easier than other types of loans because your home is collateral.

Common Costs And Fees To Expect

Origination fees are charges lenders apply for processing your loan. These fees usually range from 0.5% to 1.5% of the loan amount. They cover administrative tasks and paperwork.

Appraisal costs pay for a professional evaluation of your home’s value. This helps the lender decide how much money to lend. Typical appraisal fees are $300 to $500, depending on location and property size.

Closing costs include various fees needed to finalize the loan. These can cover title insurance, recording fees, and attorney charges. Expect to pay about 2% to 5% of the loan amount in closing costs.

Smart Tips To Unlock Savings

Compare loan rates from different lenders. This helps find the best deal. Even a small rate change can save you a lot.

Boost your credit score before applying. Pay bills on time and reduce debts. A higher score means lower interest rates.

Pick a loan term that fits your budget. Shorter terms save on interest but cost more monthly. Longer terms lower payments but add more interest.

Timing matters. Interest rates and home values can change. Watch market trends to apply when rates are low and values are steady.

Risks Of Taking A Property Equity Loan

Potential Foreclosure is a serious risk with property equity loans. Missing payments can lead to losing your home. Lenders have the right to take ownership if you don’t pay back the loan.

Impact on Future Home Sales can be significant. A property equity loan adds a lien on your home. This can make selling your home harder or slower. Buyers may be wary of properties with extra loans.

Variable Interest Rate Risks mean your monthly payments can change. Rates might start low but can rise over time. Higher rates increase your loan cost and monthly bills. This can strain your budget unexpectedly.

Alternatives To Property Equity Loans

Home Equity Line of Credit (HELOC) lets you borrow money using your home’s value. You can withdraw funds as needed, paying interest only on what you use. The rate can change over time, so monthly payments may vary.

Cash-Out Refinance replaces your current mortgage with a new one for a higher amount. You get the difference in cash. It may have a lower interest rate than other loans but increases your mortgage balance.

Personal Loans do not use your home as security. They are quick and easy to get but usually have higher interest rates. The loan amount is fixed, and payments remain the same.

How To Apply For A Property Equity Loan

Gather important documents before applying for a property equity loan. These include proof of income, bank statements, and property details. Lenders need these to check your financial health.

Compare loan estimates carefully. Look at the interest rates, fees, and loan terms. Choose the option that suits your budget and needs best.

Work closely with lenders. Ask questions if anything is unclear. Getting clear answers helps avoid surprises later. Always read the fine print before signing any agreement.

Frequently Asked Questions

How Much Would A $100,000 Home Equity Loan Cost Per Month?

A $100,000 home equity loan typically costs $450 to $600 per month. Payments depend on interest rates and loan terms. Use a loan calculator for precise estimates based on your rate and term.

What Would My Payment Be On A $50,000 Home Equity Loan?

Your payment on a $50,000 home equity loan depends on the interest rate and loan term. For example, at 6% over 15 years, payments would be about $421 per month. Use a home equity loan calculator for precise estimates based on your rate and term.

Do You Need 20% Equity For A Heloc?

You typically need at least 20% equity in your home to qualify for a HELOC. Lenders want sufficient equity to reduce risk.

What Does Dave Ramsey Say About A Home Equity Loan?

Dave Ramsey advises against home equity loans due to high risk and potential for losing your home. He prefers paying cash or avoiding debt.

Conclusion

Understanding your property equity loan estimate helps you plan better. It shows how much you can borrow and what costs to expect. Comparing different estimates saves money and avoids surprises. Always check the loan terms carefully before deciding. This way, you protect your investment and manage payments wisely.

Taking time to review your options leads to smart financial choices. Keep your goals clear and stay informed throughout the process. Property equity loans can support your needs if handled with care.