Are you looking to tap into the value of your home without taking out a traditional loan? Understanding home equity credit line rates could be the key to unlocking flexible funds for renovations, emergencies, or other big expenses.

But with rates that can change and vary from lender to lender, how do you make sure you’re getting the best deal? You’ll discover what drives these rates, how to compare offers, and tips to secure terms that work best for your budget.

Keep reading to take control of your home equity and make smarter financial choices today.

Home Equity Credit Lines

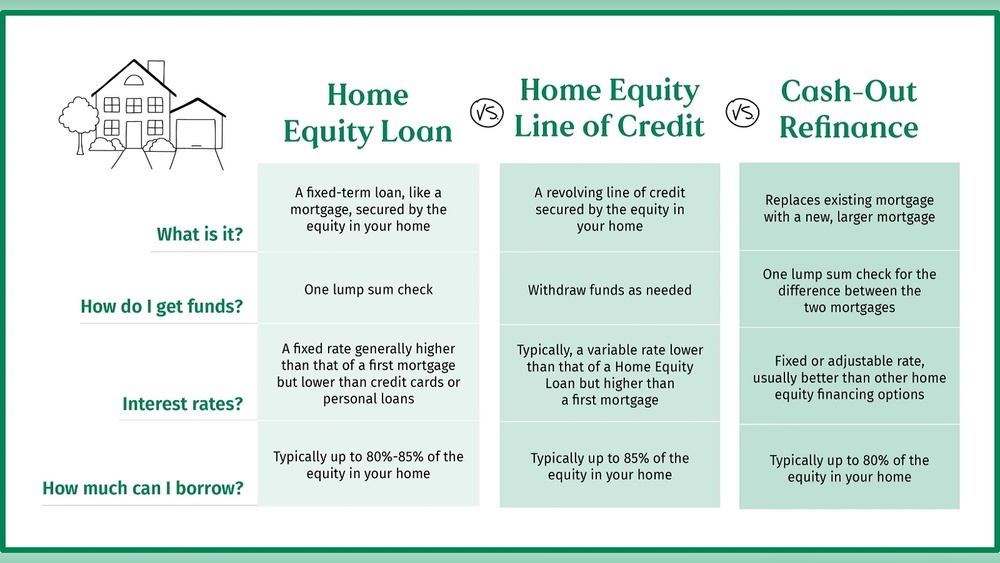

A HELOC is a loan that lets you borrow money using your home’s value. It works like a credit card with a limit based on your home equity. You can borrow and repay money during the draw period, usually 5 to 10 years. After that, you repay the balance over time.

A HELOC differs from a home equity loan. A home equity loan gives you a lump sum with fixed payments. HELOCs have variable interest rates, which can change each month. This means your payments can go up or down.

- Flexibility: Borrow only what you need when you need it.

- Lower initial rates: HELOCs often start with lower interest rates than other loans.

- Interest-only payments: During the draw period, you may pay only interest.

- Use for many purposes: Home repairs, education, emergencies, and more.

Current Heloc Rates

Most HELOC rates use a variable rate structure. This means the interest rate can change each month. It usually moves with the U.S. Prime Rate. This makes payments flexible but can increase over time.

Typical APR ranges for HELOCs vary from about 6% to 12%. The exact rate depends on your credit score, loan amount, and lender. Lower credit scores often mean higher APRs.

| Rate Type | Description | Pros | Cons |

|---|---|---|---|

| Variable | Rate changes with market | Usually lower at first, flexible | Payments can rise unexpectedly |

| Fixed | Rate stays the same | Stable payments, easy to budget | Often higher starting rate |

Top Lenders In Austin

Bank of America offers competitive HELOC rates with flexible borrowing options. Their rates often start low but can change monthly, based on the U.S. Prime Rate. This makes it easier to manage expenses like home repairs or education costs.

Navy Federal Credit Union provides advantages such as lower fees and member-focused service. Their HELOC rates are usually attractive for military members and their families. The credit union emphasizes personalized support and easy access to funds.

U.S. Bank and other regional lenders provide local options for HELOCs. These banks may offer customized rates and terms suitable for homeowners in Austin. Regional lenders often understand local market needs better, giving borrowers more choices.

Factors Affecting Rates

Credit score plays a big role in setting home equity credit line rates. A higher credit score usually means lower interest rates. Lenders see borrowers with good credit as less risky, so they offer better terms. On the other hand, low scores may lead to higher rates or tougher approval.

Loan-to-value (LTV) ratio measures the loan amount compared to your home’s value. A lower LTV ratio often results in lower rates. This is because the lender has more equity as a cushion. If the LTV is high, lenders may charge more to cover their risk.

The prime rate is the base interest rate banks use for many loans, including HELOCs. If the prime rate goes up, your HELOC rate will likely increase too. When it falls, rates usually drop. Most HELOCs have variable rates tied to this prime rate.

How To Compare Rates

Online tools help find and compare home equity credit line rates quickly. They show current rates from many lenders side-by-side. These tools often include calculators to estimate monthly payments based on your loan amount and term.

Evaluating lender terms is important beyond just rates. Look for details like how long the introductory rate lasts and if the rate is fixed or variable. Also, check if the lender allows you to borrow only what you need or requires a minimum draw.

Fees and costs affect the total loan price. Common fees include application fees, annual fees, and closing costs. Some lenders waive fees to attract customers. Compare these fees along with the interest rate to find the best deal.

Maximizing Savings

Locking in low rates can save a lot of money over time. Rates tend to change, so securing a low rate early is smart. Many lenders offer a fixed-rate option for peace of mind. This helps avoid sudden payment increases.

Flexible repayment plans allow you to manage payments easily. Some plans let you pay interest only at first, then pay principal later. This can keep monthly bills lower when money is tight. Choose a plan that fits your budget and goals.

Timing your application matters. Rates often rise or fall with economic changes. Applying when rates are low can lock in better terms. Also, avoid applying when your credit score is low or your debt is high. Good timing can mean better savings.

Risks To Consider

Variable rate fluctuations mean your payments can change monthly. This depends on the U.S. Prime Rate. A rise in rates makes borrowing more expensive. A drop lowers your payments, but it can be unpredictable. Always expect changes over time.

Your home equity is the value of your home minus what you owe. Using a HELOC reduces this equity. If home prices fall, you might owe more than your home is worth. This risk is important to remember before borrowing.

| Potential Fees | Description |

|---|---|

| Application Fee | Charged when you apply for the HELOC. |

| Annual Fee | Some lenders charge yearly fees for having the line open. |

| Closing Costs | Costs for processing and setting up the loan. |

| Early Closure Fee | Fee if you pay off or close the HELOC early. |

Calculating Your Heloc

Estimating Available Equity starts with knowing your home’s current value. Subtract the amount you still owe on your mortgage from that value. The result is your available equity. This number helps determine how much you can borrow.

Using HELOC Calculators online can make this easier. Enter your home’s value, mortgage balance, and lender limits. The calculator shows your potential credit line and monthly payments.

Budgeting for Payments means planning for monthly costs. HELOC rates usually change, so payments can vary. Be sure your budget can handle higher payments if rates rise.

Frequently Asked Questions

What Is The Monthly Payment On A $50,000 Home Equity Line Of Credit?

Monthly payments on a $50,000 HELOC vary based on interest rates and repayment terms. Typically, payments range from $200 to $400. Variable rates affect monthly costs, so check current rates with lenders like Bank of America or Navy Federal Credit Union for precise estimates.

What Is The Normal Interest Rate On A Home Equity Line Of Credit?

The normal interest rate on a home equity line of credit (HELOC) typically ranges from 6% to 14%, depending on credit and market conditions. Most HELOCs feature variable rates tied to the U. S. Prime Rate, which can change monthly.

Will Home Interest Rates Ever Get To 3% Again?

Home interest rates may reach 3% again, but it depends on economic conditions and Federal Reserve policies. Rates fluctuate over time.

Is It Smart To Do A Home Equity Line Of Credit?

A home equity line of credit (HELOC) can be smart for flexible borrowing and lower interest rates. Assess your risk tolerance and repayment ability before proceeding.

Conclusion

Choosing the right home equity credit line rate can save money over time. Rates often change with the market, so check them regularly. Comparing offers from different lenders helps find the best deal. Understand the terms clearly before borrowing to avoid surprises.

Use available tools to see current rates in your area. A well-chosen HELOC can support home improvements or emergencies. Stay informed and borrow responsibly to manage your finances well.