If you’re considering tapping into your home’s equity, understanding your potential payments is key—especially when dealing with a variable HELOC. You want to know how much your monthly payments might be, and how changes in interest rates could affect your budget.

That’s where a variable HELOC payment estimate becomes essential. You’ll discover how to estimate your payments, what factors influence them, and how to plan ahead so you feel confident and in control of your finances. Keep reading to make smart decisions about your home equity line of credit.

Variable Heloc Basics

A Variable HELOC is a home equity line of credit with a rate that can change. The interest rate depends on an index plus a margin set by the lender. This means your payments can go up or down over time.

Variable rates affect payments because when rates rise, monthly payments increase. When rates fall, payments go down. This makes budgeting harder, but can save money if rates drop.

| Feature | Fixed Rate | Variable Rate |

|---|---|---|

| Interest Rate | Stays the same | Changes over time |

| Monthly Payments | Predictable | Can rise or fall |

| Risk Level | Lower | Higher |

| Potential Savings | None | Possible if rates drop |

Factors Influencing Heloc Payments

Credit limit sets the maximum amount you can borrow. During the draw period, payments often cover only interest. Borrowing less than the limit lowers monthly payments.

Interest rates can change over time. Variable rates mean payments may go up or down. Small rate changes can affect your payment a lot.

The repayment period defines how long you have to pay back. Shorter periods mean higher monthly payments but less total interest. Longer terms lower monthly payments but increase total interest paid.

Estimating Your Heloc Payments

Online calculators help estimate HELOC payments quickly. They ask for the loan amount, interest rate, and loan term. Then, they show your monthly payment.

Interest-only payments are usually lower. You pay just the interest each month. The principal stays the same until you start paying it back.

Estimating principal and interest payments means paying both parts each month. This amount is higher but reduces your loan balance over time.

| Payment Type | Description | Monthly Payment |

|---|---|---|

| Interest-Only | Pay just the interest, no principal | Lower |

| Principal & Interest | Pay both principal and interest | Higher |

Tips For Accurate Payment Planning

Interest rates on a variable HELOC can change often. Keep track of these changes to avoid surprises. Check your lender’s updates regularly and note any rate adjustments.

Plan your budget with payment variations in mind. Set aside extra money for months when payments rise. This helps keep your finances steady without stress.

Making early principal payments can lower your overall interest. Paying extra on your loan reduces the amount you owe faster. This can save you money and shorten your loan term.

Managing Payment Risks

Interest rates on variable HELOCs can rise, increasing monthly payments. Preparing for these changes helps avoid surprises. Set a budget that includes possible higher payments to stay safe.

Payment alerts are useful. They notify you before payment due dates or if amounts change. Alerts prevent late fees and keep your account on track.

Refinancing might lower your rate or fix payments. Check your credit score and loan terms. Compare offers from different lenders to find better deals. Refinancing can bring peace of mind and more predictable costs.

Tools And Resources

Top HELOC payment calculators help estimate monthly costs quickly. Popular tools include those from Bank of America, U.S. Bank, and Bellco Credit Union. These calculators let users input loan amount, interest rate, and term to see estimated payments. They often show options for interest-only or principal plus interest payments. Using these tools can simplify budgeting for your HELOC.

Financial apps help track payments and balances easily. Apps like Mint, YNAB, and Personal Capital allow users to set reminders and view payment history. These apps provide notifications to avoid missed payments. They also help monitor how changes in interest rates affect monthly costs.

Consulting financial advisors offers personalized advice. Advisors can explain how variable rates impact payments over time. They help create a plan that fits your budget and goals. Professional guidance ensures you understand all loan terms and risks before borrowing.

Frequently Asked Questions

What Is The Average Heloc Payment On $100,000?

The average HELOC payment on $100,000 varies by interest rate and term. Typically, expect $300 to $600 monthly. Interest-only payments start lower, around $200, increasing after the draw period. Variable rates cause fluctuations, so use a HELOC calculator for precise estimates.

Is A Variable Rate Heloc A Good Idea?

A variable rate HELOC offers lower initial rates but risks rising payments if interest rates increase. It suits those comfortable with rate fluctuations.

What Does Dave Ramsey Say About Paying Off Heloc?

Dave Ramsey advises paying off your HELOC quickly to avoid high interest costs. He suggests using the debt snowball method for faster repayment.

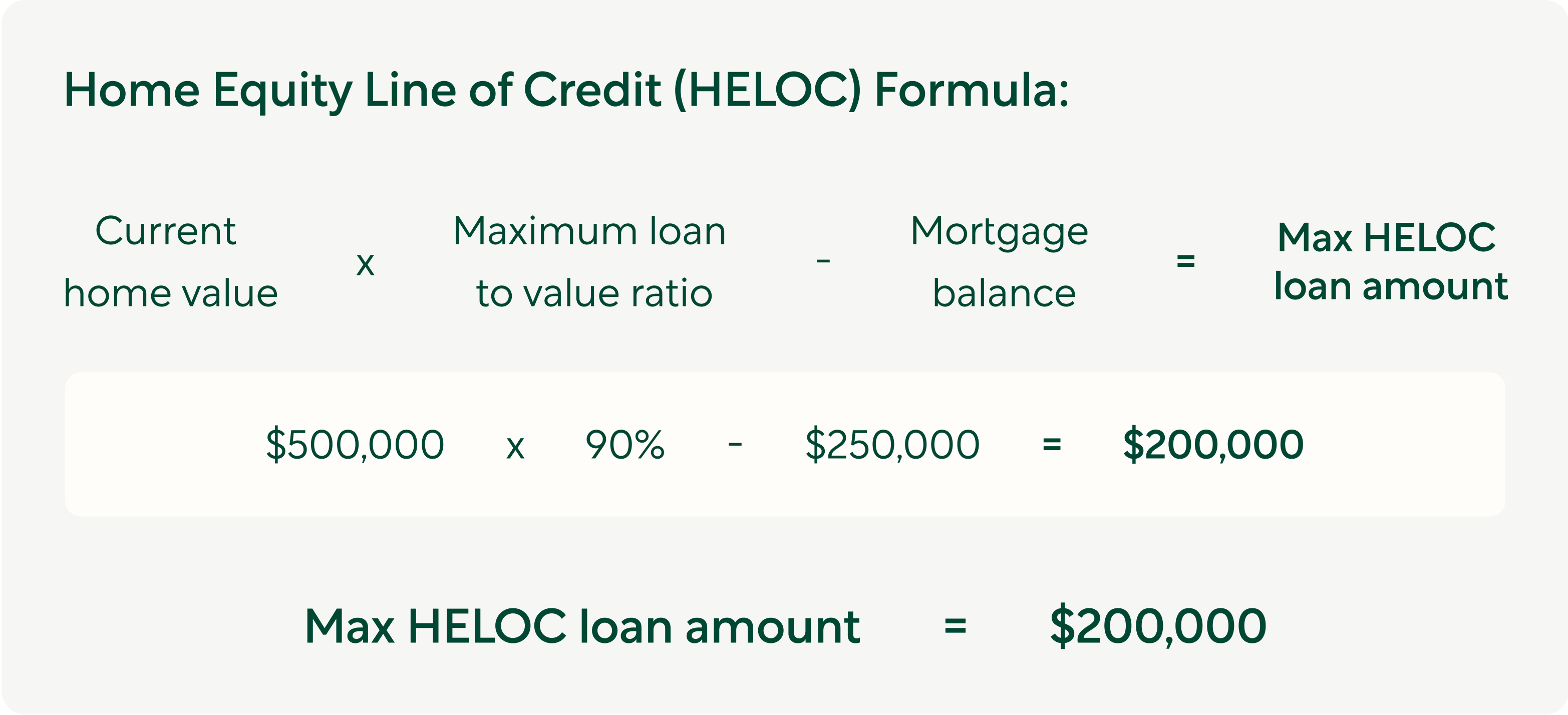

What Is The 80 Rule For Heloc?

The 80 rule for HELOC means you can borrow up to 80% of your home’s appraised value minus your mortgage balance.

Conclusion

Estimating your variable HELOC payments helps you plan your budget better. Payments can change with interest rate shifts, so stay informed. Using a payment calculator gives a clear idea of monthly costs. This helps avoid surprises and manage your finances wisely.

Keep track of your balance and rates regularly. A good estimate supports smarter borrowing decisions. Understanding your payment estimate leads to better control over your home equity loan.