Have you ever wondered how to unlock the hidden value of your home to fund your dreams or handle unexpected expenses? An equity cash out refinance might be the key you’re looking for.

This smart financial move lets you tap into your home’s equity and turn it into cash, all while replacing your existing mortgage with a new loan. Whether you want to renovate your home, pay off high-interest debt, or invest in new opportunities, understanding how a cash out refinance works can open doors you didn’t know existed.

Keep reading to discover how you can make your home equity work for you, what to watch out for, and the steps to take next. Your financial freedom could be just a refinance away.

Cash-out Refinance Basics

A cash-out refinance replaces your current mortgage with a new loan. The new loan is larger than the old one. You receive the difference in cash after paying off the old mortgage.

The loan-to-value (LTV) ratio is important. It compares your loan amount to your home’s value. Most lenders allow up to 80% LTV for cash-out refinancing. For example, if your home is worth $400,000, you can borrow up to $320,000.

Eligibility depends on several factors:

- Credit score: Usually at least 620 is needed.

- Debt-to-income ratio (DTI): Should be below 43% in most cases.

- Equity: You must have enough equity in your home to cash out.

- Employment and income: Steady income and job history matter.

Benefits Of Cash-out Refinance

Accessing home equity means using the value built in your house.

Cash-out refinance lets you borrow money using your home’s worth.

Lower interest rates often make this option cheaper than other loans.

You can get a better deal compared to credit cards or personal loans.

Debt consolidation opportunities help you combine several debts into one.

This can simplify payments and lower monthly costs.

Using this method, homeowners can improve their financial situation.

Risks And Drawbacks

Increased loan balance means you owe more money than before. This can make it harder to pay off the loan quickly. A bigger loan might also mean paying more interest over time.

Potentially higher monthly payments can strain your budget. The new loan might have a higher interest rate or longer term, leading to larger payments. This can reduce your cash flow each month.

The impact on credit score can be negative. Applying for a cash-out refinance usually involves a credit check. Also, increasing your debt could lower your credit score temporarily.

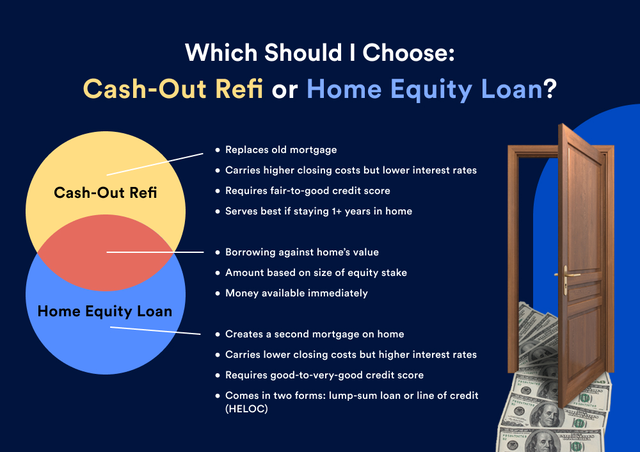

Cash-out Refinance Vs Heloc

Cash-out refinance replaces your current mortgage with a new loan. You get a lump sum of cash at closing. This loan pays off your old mortgage first. Any extra money goes to you. The new loan may have different terms like interest rate or length.

HELOC works like a credit card. It gives you a line of credit based on your home equity. You borrow and repay as you need, up to a limit. You pay interest only on what you use. HELOCs usually have variable interest rates.

| Cash-Out Refinance | HELOC | |

|---|---|---|

| Loan Structure | One new loan, pays off old mortgage | Line of credit, borrow as needed |

| Cost | Closing costs, usually higher upfront | Lower upfront costs, variable interest |

| Best Use | Large, one-time cash needs | Ongoing or flexible spending |

Qualifying For Cash-out Refinance

Credit score is a key factor to qualify for a cash-out refinance. Most lenders want a score of at least 620, but higher scores get better rates. Scores below this may face higher interest or denial.

Debt-to-Income (DTI) ratio shows how much you owe versus your income. Lenders usually want a DTI below 43%. This means your monthly debts should not exceed 43% of your monthly income.

| Requirement | Typical Limit |

|---|---|

| Credit Score | 620 or higher |

| Debt-to-Income Ratio | Less than 43% |

| Loan-to-Value (LTV) after refinance | Typically 80% or less |

An appraisal is needed to determine home value. Lenders require this to decide how much cash you can take out. You must provide proof of income, assets, and debts to support your loan application.

Steps To Apply

Start by knowing your home’s equity. This is the difference between your home’s value and what you owe. Use online tools or get a professional appraisal. This helps you see how much money you can borrow.

Shop around for lenders and rates. Compare offers from banks, credit unions, and online lenders. Look at interest rates, fees, and loan terms. Choose the lender that fits your budget and needs best.

Prepare your application carefully. Gather documents like proof of income, credit report, and home appraisal. Fill out the application honestly and completely. This speeds up the approval process and helps avoid delays.

Smart Strategies To Use Cash-out Funds

Using cash-out refinance funds for home improvements can increase your home’s value. Simple upgrades like new paint, kitchen remodels, or bathroom updates often offer great returns. This makes your property more attractive if you plan to sell later.

Investing in real estate with cash-out money allows you to buy rental properties. Rental income can help cover mortgage payments and build wealth over time. This strategy works well for long-term financial growth.

Paying off high-interest debt such as credit cards or personal loans can save you money. Lower interest rates on your mortgage mean smaller monthly payments. This reduces financial stress and improves your credit score.

Common Mistakes To Avoid

Overborrowing against your equity can lead to serious financial trouble. Taking out too much money leaves less equity in your home. This reduces your safety net if home values drop or emergencies arise.

Ignoring closing costs is a common mistake. These fees can add thousands to your loan. Always include closing costs in your budget to avoid surprises and ensure the refinance is truly worth it.

Not considering the long-term financial impact may hurt your future. Cash-out refinancing often raises your monthly payments or extends your loan term. Think about how this affects your budget and financial goals before proceeding.

Local Insights: Austin, Texas Market

Home equity in Austin has been rising steadily as property values grow. Many homeowners have significant equity to consider cash-out refinancing. The average equity available varies by neighborhood but remains strong across the city.

| Popular Lenders | Loan Types | Interest Rates |

|---|---|---|

| U.S. Bank | Cash-Out Refinance, HELOC | 3.5% – 4.2% |

| Wells Fargo | Cash-Out Refinance | 3.6% – 4.3% |

| Navy Federal Credit Union | Cash-Out Refinance | 3.4% – 4.1% |

Austin homeowners must consider local regulations on refinancing. Texas law protects consumers with clear disclosure rules. Tax rules may affect the benefits of cash-out refinancing. For example, interest deductions depend on how the funds are used. Always check with a tax advisor before proceeding.

Resources And Tools

Mortgage calculators help estimate monthly payments and interest costs. They show how much cash you might get from a refinance.

Lender comparison guides list different lenders side by side. They show rates, fees, and terms. This helps choose the best deal.

Financial planning assistance offers advice on managing money after refinancing. Experts can explain how cash-out refinance affects budgets and taxes.

| Resource | Purpose |

|---|---|

| Mortgage Calculators | Estimate payments and potential cash from refinance |

| Lender Comparison Guides | Compare interest rates, fees, and loan terms |

| Financial Planning Assistance | Help with budgeting and tax implications after refinancing |

Frequently Asked Questions

Can You Cash Out Equity When Refinancing?

Yes, you can cash out equity when refinancing by replacing your mortgage with a larger loan. This pays off your current loan and provides a lump sum of cash.

Is A Cash-out Refinance A Good Idea?

A cash-out refinance can be a good idea to access home equity for debt consolidation or home improvements. It lowers interest rates but increases loan balance and monthly payments. Evaluate your financial goals and compare options before deciding.

How Much Would A $50,000 Home Equity Loan Be A Month?

A $50,000 home equity loan’s monthly payment varies by interest rate and term. For 5% interest over 15 years, expect about $395.

How Much Equity For A Cash-out Refinance?

Lenders typically allow cash-out refinancing up to 80% loan-to-value (LTV). This means you can borrow 80% of your home’s appraised value minus your current mortgage balance. Requirements vary by lender, credit score, and debt-to-income ratio.

Conclusion

Equity cash out refinance can help you access your home’s value easily. It replaces your current mortgage with a new one. You get cash to use for various needs like repairs or debt. Make sure to compare rates and terms before deciding.

Understanding the pros and cons is important. Talk to a trusted lender to find the best option. This choice can fit many financial goals if used wisely. Keep your budget in mind to avoid future problems. Take time to learn and plan carefully.